Canada Emergency Response Benefit

What is the Canada Emergency Response Benefit

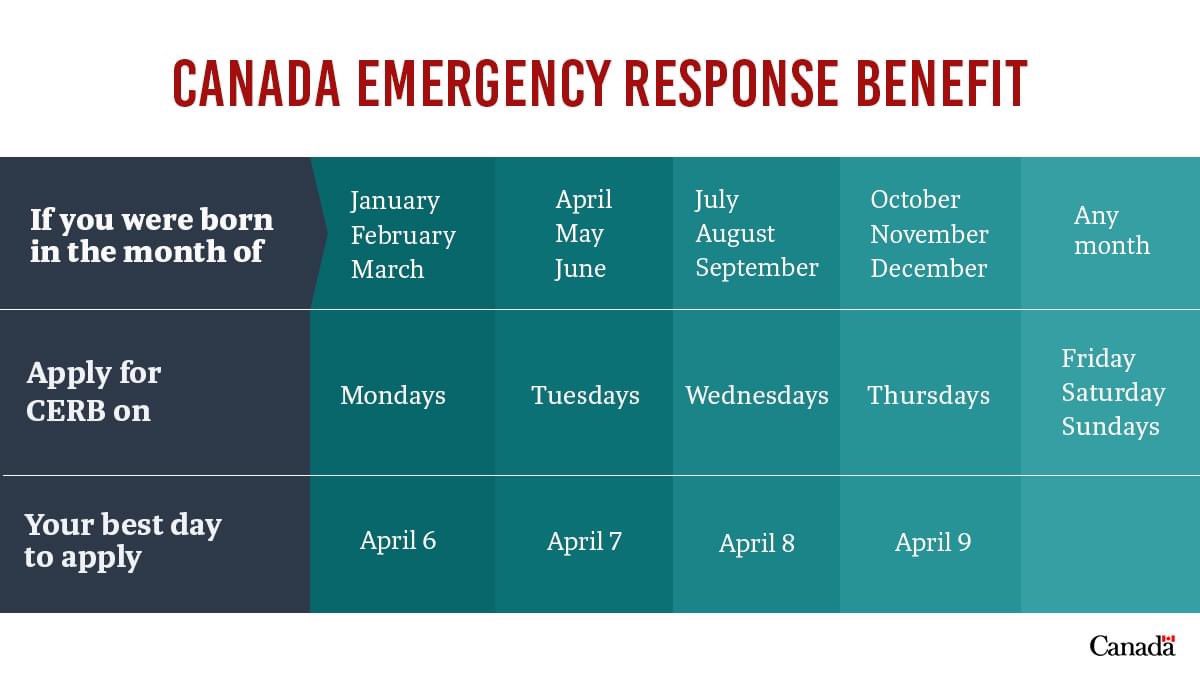

If you have stopped working because of COVID-19, the Canada Emergency Response Benefit (CERB) may provide you with temporary income support. The CERB provides $500 a week for up to 16 weeks.

Who is eligible

The benefit will be available to workers:

- Residing in Canada, who are at least 15 years old;

- Who have stopped working because of COVID-19 and have not voluntarily quit their job or are eligible for EI regular or sickness benefits;

- Who had income of at least $5,000 in 2019 or in the 12 months prior to the date of their application; and

- Who are or expect to be without employment or self-employment income for at least 14 consecutive days in the initial four-week period. For subsequent benefit periods, they expect to have no employment or self-employment income.

How to apply

To deliver payments to Canadians in a fast and easy way, the CERB is being jointly delivered by Service Canada and the Canada Revenue Agency.

To begin the application process, please answer a few simple questions. The answers you provide will help us direct you to the service option that best fits your situation.

Please read these questions and answers for more details.

Special Goods and Services Tax credit payment

The federal government is providing a one-time special payment starting April 9 through the Goods and Services Tax credit for low- and modest-income families.The average additional benefit will be close to $400 for single individuals and close to $600 for couples.There is no need to apply for this payment. If you are eligible, you will get it automatically.

Extra time to file income tax returns

The filing due date for 2019 income tax returns for individuals has been deferred until June 1, 2020. Any new income tax balances due, or instalments, are also being deferred until after August 31, 2020 without incurring interest or penalties.Consult all tax and payment dates

Note: If you expect to receive benefits under the Goods and Services Tax credit or the Canada Child Benefit, we encourage you not to delay filing your 2019 income tax return to ensure that your entitlements are properly determined.

Mortgage support

Canadian banks have committed to work with their customers on a case-by-case basis to find solutions to help them manage hardships caused by COVID-19. This includes permitting lenders to defer up to six monthly mortgage payments (interest and principal) for impacted borrowers. Canadians who are impacted by COVID-19 and experiencing financial hardship as a result should contact their financial institution regarding flexibility for a mortgage deferral. This gives flexibility to be available − when needed − to those who need it the most. You are encouraged to visit your bank’s website for the latest information, rather than calling or visiting a branch.Consult your bank’s dedicated COVID-19 page

Contact your financial institution for further mortgage assistance.

The Canada Mortgage and Housing Corporation and other mortgage insurers offer tools to lenders that can assist homeowners who may be experiencing financial difficulty. These include payment deferral, loan re-amortization, capitalization of outstanding interest arrears and other eligible expenses, and special payment arrangements.Canada’s mortgage insurers are committed to providing homeowners with solutions to mitigate temporary financial hardship related to COVID-19. This includes permitting lenders to defer up to six monthly mortgage payments (interest and principal) for impacted borrowers. Deferred payments are added to the outstanding principal balance and subsequently repaid throughout the life of the mortgage.Learn more: Financial Consumer Agency of Canada (FCAC)

The Canada Emergency Wage Subsidy

What It Means for Canadian Businesses

To help businesses keep and return workers to their payroll through the challenges posed by the COVID-19 pandemic, the Prime Minister, Justin Trudeau, proposed the new Canada Emergency Wage Subsidy. This would provide a 75 per cent wage subsidy to eligible employers for up to 12 weeks, retroactive to March 15, 2020.

This wage subsidy aims to prevent further job losses, encourage employers to re-hire workers previously laid off as a result of COVID-19, and help better position Canadian companies and other employers to more easily resume normal operations following the crisis. While the Government has designed the proposed wage subsidy to provide generous and timely financial support to employers, it was done with the expectation that employers will do their part by using the subsidy in a manner that supports the health and well-being of their employees.

Eligible Employers

Eligible employers would include individuals, taxable corporations, and partnerships consisting of eligible employers as well as non‑profit organizations and registered charities.

Public bodies would not be eligible for this subsidy. Public bodies include municipalities and local governments, Crown corporations, public universities, colleges, schools and hospitals.

This subsidy would be available to eligible employers that see a drop of at least 30 per cent of their revenue (see Eligible Periods). In applying for the subsidy, employers would be required to attest to the decline in revenue.

Calculating Revenues

An employer’s revenue for this purpose would be its revenue from its business carried on in Canada earned from arm’s-length sources. Revenue would be calculated using the employer’s normal accounting method, and would exclude revenues from extraordinary items and amounts on account of capital.

For non-profits and charities, the government will continue to work with the sector to ensure the definition of revenue is appropriate to their specific circumstances.

Amount of Subsidy

The subsidy amount for a given employee on eligible remuneration paid between March 15 and June 6, 2020 would be the greater of:

- 75 per cent of the amount of remuneration paid, up to a maximum benefit of $847 per week; and

- the amount of remuneration paid, up to a maximum benefit of $847 per week or 75 per cent of the employee’s pre-crisis weekly remuneration, whichever is less.

Further guidance with respect to how to define pre-crisis weekly remuneration for a given employee will be provided in the coming days.

In effect, employers may be eligible for a subsidy of up to 100 per cent of the first 75 per cent of pre-crisis wages or salaries of existing employees. These employers would be expected where possible to maintain existing employees’ pre-crisis employment earnings.

Employers will also be eligible for a subsidy of up to 75 per cent of salaries and wages paid to new employees.

Eligible remuneration may include salary, wages, and other remuneration. These are amounts for which employers would generally be required to withhold or deduct amounts to remit to the Receiver General on account of the employee’s income tax obligation. However, it does not include severance pay, or items such as stock option benefits or the personal use of a corporate vehicle.

A special rule will apply to employees that do not deal at arm’s length with the employer. The subsidy amount for such employees will be limited to the eligible remuneration paid in any pay period between March 15 and June 6, 2020, up to a maximum benefit of $847 per week or 75 per cent of the employee’s pre-crisis weekly remuneration.

There would be no overall limit on the subsidy amount that an eligible employer may claim.

Employers must make their best effort to top-up employees’ salaries to bring them to pre-crisis levels.

Eligible Periods

Eligibility would generally be determined by the change in an eligible employer’s monthly revenues, year-over-year, for the calendar month in which the period began. The amount of wage subsidy (provided under the COVID-19 Economic Response Plan) received by the employer in a given month would be ignored for the purpose of measuring year-over-year changes in monthly revenues.

- For example, if revenues in March 2020 were down 50 per cent compared to March 2019, the employer would be allowed to claim the Canadian Emergency Wage Subsidy (as calculated above) on remuneration paid between March 15 and April 11, 2020.

The table below outlines each claiming period and the period in which it has a decline in revenue of 30 per cent or more.

| Claiming period | Reference period for eligibility | |

|---|---|---|

| Period 1 | March 15 – April 11 | March 2020 over March 2019 |

| Period 2 | April 12 – May 9 | April 2020 over April 2019 |

| Period 3 | May 10 – June 6 | May 2020 over May 2019 |

For eligible employers established after February 2019, eligibility would be determined by comparing monthly revenues to a reasonable benchmark.

How to Apply

Eligible employers would be able to apply for the Canada Emergency Wage Subsidy through the Canada Revenue Agency’s My Business Account portal as well as a web-based application. Employers would have to keep records demonstrating their reduction in arm’s-length revenues and remuneration paid to employees. More details about the application process will be made available shortly.

Canada Emergency Business Account

The new Canada Emergency Business Account will provide interest-free loans of up to $40,000 to small businesses and not-for-profits, to help cover their operating costs during a period where their revenues have been temporarily reduced.

To qualify, these organizations will need to demonstrate they paid between $50,000 to $1 million in total payroll in 2019.

This program will roll out in mid-April, and interested businesses should work with their current financial institutions.